Exploring the potential of emerging blockchains in stablecoin adoption: Who can outperform Ethereum?

Original Article Title: "Beyond Ethereum: Exploring the Potential of Emerging Blockchains in Stablecoin Adoption"

Original Source: Aquarius

Background

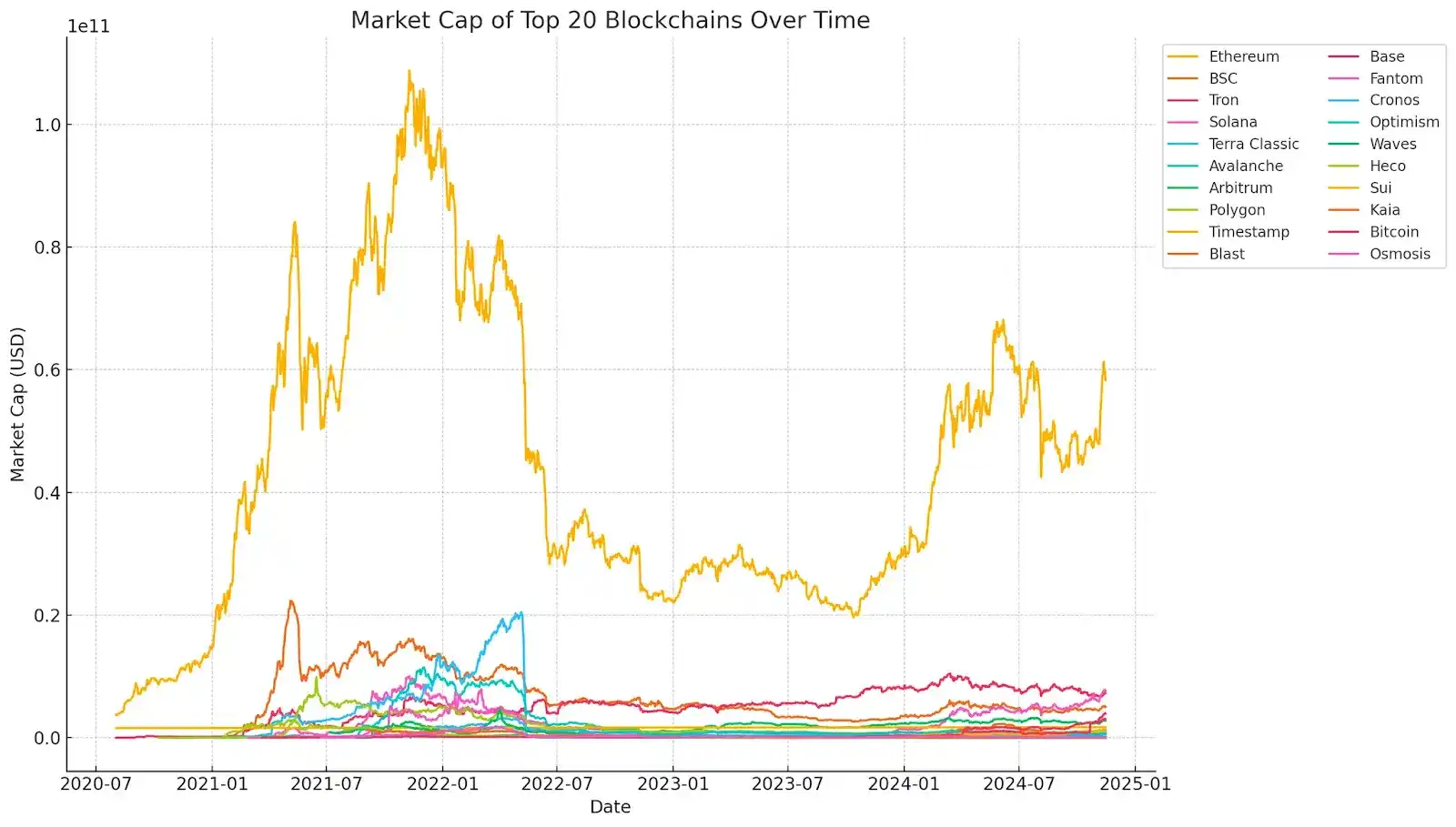

The stablecoin market has experienced rapid growth, becoming a significant force in the digital economy, even competing with the traditional financial network. According to Coinbase's research, the total trading volume of stablecoins in 2023 exceeded $10.8 trillion. After excluding "non-natural" trades (such as bot-driven or automated trades), the actual trading volume was around $2.3 trillion. This adjusted data reflects an organic annual growth rate of stablecoins reaching 17%, highlighting the increasingly important role of stablecoins in retail and institutional finance. The following chart provides a visual insight into the current landscape and growth trajectory of stablecoins in major blockchain ecosystems.

This chart shows the overall market trend of the top 20 blockchains from 2020 to 2025. Ethereum stands out, with a market value exceeding $1 trillion at its peak, dominating the entire blockchain ecosystem. Such a high market value is closely related to Ethereum's role as the primary platform for DeFi and stablecoin issuance, allowing it to maintain a strong position even during market fluctuations. Other blockchains (such as BSC, Tron, and Solana) have relatively lower market values but show stable performance. Particularly Tron and BSC demonstrate a stable growth trend, highlighting their role as alternative platforms for stablecoins and DeFi, especially in regions and applications where transaction costs and speed are crucial.

Notably, emerging platforms like Arbitrum, Sui, and Optimism have seen gradual market value growth, indicating an increasing adoption rate. This growth trajectory suggests that as these ecosystems mature, they may challenge existing leaders by meeting specific needs or providing competitive transaction efficiency. The data indicates that while Ethereum dominates in overall market value, other blockchains are attracting users and developers, hinting at a potential shift in stablecoin activity as the ecosystem matures.

This chart provides a more detailed view of the market capitalization trends of the top 20 blockchains' stablecoins. Ethereum leads with a stablecoin market capitalization of over $80 billion, reflecting its role as a key platform for stablecoins such as USDT, USDC, and DAI. Ethereum's massive market capitalization supports its position as a stablecoin hub, with demand mainly coming from DeFi applications and institutional users seeking compliant stablecoins. However, Tron emerges as a strong competitor with a stablecoin market capitalization of around $40 billion. Tron's appeal lies in its low transaction fees and fast processing speed, making it particularly popular in high-frequency trading scenarios such as remittances and cross-border payments.

Other blockchains (such as BSC, Terra Classic, and Solana) have relatively smaller stablecoin market capitalizations but play a crucial role in a diversified stablecoin ecosystem. For example, BSC has a stablecoin market capitalization of around $20 billion, attracting DeFi projects and retail users seeking lower fees than Ethereum. Smaller blockchains (like Algorand and Stellar) position themselves as niche platforms for stablecoins, often targeting specific use cases such as cross-border payments and small-value transactions.

Current Leaders

Ethereum: The Steadfast Leader

Ethereum is commonly seen as a cornerstone of decentralized finance (DeFi) and remains the dominant chain for stablecoin activity, with a stablecoin market capitalization exceeding $80 billion. Several factors contribute to Ethereum's continued leadership in the stablecoin ecosystem:

· Mature and Interconnected DeFi Ecosystem: Ethereum's extensive and mature DeFi ecosystem includes prominent protocols like Uniswap, Compound, and Aave, which heavily rely on stablecoin liquidity in their operations. Stablecoins are vital for liquidity pools, lending, and yield farming, making Ethereum an indispensable platform for users seeking comprehensive DeFi services.

· Institutional and Regulatory Trust: Stablecoins on Ethereum (especially USDC and DAI) have gained regulatory approval and institutional trust. With more institutions entering the crypto space, Ethereum's reputation as a secure and decentralized network makes it an ideal choice for compliant, institutional-grade stablecoins. Circle's USDC and MakerDAO's DAI are key native stablecoins on Ethereum, serving as pillars of trust in the ecosystem.

· Diverse Stablecoins and Use Cases: Ethereum hosts a wide range of stablecoins, including fiat-backed stablecoins like USDT and USDC, as well as algorithmic and decentralized stablecoins like DAI. This diversity allows Ethereum users to choose the stablecoin that best suits their risk tolerance, regulatory requirements, and preferences. For example, DAI is uniquely attractive due to its lack of direct fiat collateralization, aligning with the decentralized values cherished by the Ethereum community.

· Layer 2 Solutions Addressing Scalability Issues: Ethereum faces scalability challenges, with high Gas fees limiting small users' participation in DeFi. However, layer 2 solutions such as Arbitrum, Optimism, and zk-Rollups are significantly reducing transaction costs and increasing throughput, allowing Ethereum to maintain its leadership in stablecoin use cases without compromising decentralization.

As Ethereum continues to develop its layer 2 ecosystem and fully transition to Ethereum 2.0, its dominant position in the stablecoin market is expected to persist. With regulatory clarity around stablecoins gradually emerging, institutional adoption is poised to grow, potentially leading to the launch of more fiat-backed and compliant stablecoins on Ethereum. Additionally, Ethereum's DeFi ecosystem may continue to innovate, developing new stablecoin use cases such as synthetic assets, cross-chain stablecoins, and more complex yield-generating products.

Solana: A High-Performance Ethereum Alternative

Solana is often seen as a high-performance alternative to Ethereum, known for its fast transaction speeds and low costs. While Solana's stablecoin market cap is significantly smaller than Ethereum's, it has successfully attracted a loyal user base and is increasingly popular among retail users and developers seeking cost-effective solutions.

· High-Speed Low-Cost Transactions:

Solana's unique Proof of History (PoH) consensus mechanism supports high throughput and low latency, allowing the network to process thousands of transactions per second with minimal fees. This makes Solana an ideal choice for applications requiring frequent transactions, such as micropayments and retail stablecoin transfers. Therefore, stablecoins like USDC and USDT are often used on Solana for daily payments and fast transfers within the ecosystem.

· Integration with Payment and Gaming Applications:

Solana is positioned as an ideal platform for industries like gaming and payments that have high demands for fast and inexpensive transactions. Its user-friendly development tools and support for high-performance applications make it the preferred platform for developers to build decentralized applications (dApps) that often integrate with stablecoins. For example, blockchain game Star Atlas and music streaming service Audius are leveraging Solana's speed and stability, using stablecoins as in-game currency and tipping mechanisms, respectively.

· Network Stability Issues:

Despite Solana's high performance being a major advantage, it also faces network outages and stability issues. These downtimes have led some users to question its reliability, especially in high-value transaction or institutional use cases. Solana's network resilience is still evolving, and it needs to address these technical challenges to gain full trust in the stablecoin and DeFi market.

· Partnership with USDC and Cross-Chain Solutions:

Solana's collaboration with USDC issuer Circle is a key driver for stablecoin adoption on the platform. The availability of USDC on Solana provides users with a trusted USD-backed stablecoin, enhancing Solana's appeal. Additionally, Solana is exploring cross-chain solutions that will allow assets to flow seamlessly between Solana and Ethereum, providing users with more flexibility and expanding its influence in the stablecoin market.

Solana has significant growth potential in the stablecoin space, especially if it can maintain network stability and further solidify its position in the gaming and retail payment sectors. By continuing to collaborate with USDC and exploring cross-chain capabilities, Solana is poised to attract more stablecoin transactions and DeFi applications. However, its centralized validator structure and network outage issues may limit its appeal to institutions unless these issues are addressed.

Key Conditions for Stablecoin Growth

As the appeal of stablecoins in the cryptocurrency and financial markets continues to grow, certain ecosystem features and environments are more conducive to stablecoin adoption and growth. These environments not only have technical advantages but also strategically meet the needs of retail users and institutional investors. Below are specific characteristics of blockchain ecosystems most likely to experience a stablecoin breakthrough, along with the latest market data and trends observed.

1. Low Transaction Fees

Stablecoin transactions are typically frequent and require low latency, especially in scenarios where users rely on stablecoins for everyday transactions, cross-border payments, and remittances. An ecosystem with low transaction fees and high scalability is more attractive as it can achieve economically efficient transactions without network congestion.

In a 2023 survey targeting stablecoin users, over 60% of respondents stated that transaction costs were their primary consideration when choosing a blockchain platform. Ethereum's average transaction fee often exceeds $10 during network congestion, while networks like Tron and BSC have average transaction fees below $0.10. This has attracted a significant amount of USDT migration from Ethereum to Tron, with Tron capturing approximately 30% of the USDT supply, primarily benefiting from its low fees, particularly appealing in regions with high demand for cross-border remittances. Additionally, Binance Smart Chain (BSC) continues to attract retail users to participate in its DeFi ecosystem due to transaction fees far lower than Ethereum.

A blockchain environment that provides low fees and high scalability (such as Polygon's Ethereum Layer 2 solution and Solana) is also very suitable for the growth of stablecoins. Solana can process up to 65,000 transactions per second with relatively low average fees, especially in payment and gaming applications, leading to an increase in stablecoin adoption.

2. A Robust DeFi Ecosystem with Diverse Use Cases

A robust DeFi ecosystem not only attracts stablecoin liquidity but also offers utility beyond simple transactions. In an environment with applications such as lending and yield farming, stablecoins serve as a stable medium of exchange and collateral, becoming central to various DeFi products.

Ethereum hosts over 70% of the global DeFi applications, with stablecoins accounting for nearly 50% of the Ethereum DeFi Total Value Locked (TVL). The widespread use of stablecoins is a key reason why Ethereum maintains its leadership in stablecoin adoption, despite its high fees. As of the second quarter of 2024, Ethereum's DeFi TVL is approximately $400 billion, with stablecoins such as USDC, USDT, and DAI playing a significant role.

Binance Smart Chain (BSC) also has an active DeFi ecosystem, with platforms like PancakeSwap and Venus widely using stablecoins in liquidity pools and lending markets. In 2023, BSC's DeFi TVL exceeded $5 billion, with stablecoins representing about 40% of the liquidity pools. This usability and ecosystem accessibility further encourage stablecoin adoption.

3. Interoperability

As the crypto space gradually moves towards a multi-chain ecosystem, interoperability has become a critical factor in stablecoin adoption. Stablecoins need to flow seamlessly across different blockchains to meet users' needs for transacting or holding assets across multiple chains. Ecosystems that enable easy cross-chain stablecoin transfers will benefit from increased adoption.

According to Chainalysis' 2023 report, cross-chain stablecoin transfers account for about 25% of all stablecoin transactions. Solutions like Cosmos' Inter-Blockchain Communication (IBC) protocol support stablecoin free movement across different chains within the Cosmos ecosystem, driving broader liquidity and use cases.

Cosmos and Polkadot are two major ecosystems focused on interoperability. Cosmos' IBC protocol allows blockchains within its network to interact seamlessly, enabling stablecoins to move effortlessly between chains and promoting their adoption within specific ecosystems, such as Terra's UST and other stable assets issued by Cosmos chains. Polkadot's parallel chain structure provides similar interoperability, aiding in driving stablecoin adoption across DeFi and specialized applications.

Projects like USDC also prioritize multi-chain issuance, currently supporting Ethereum, Solana, BSC, and Avalanche. By achieving cross-chain compatibility, these ecosystems can enhance the usability of stablecoins and promote broader adoption.

4. Support Regulatory Compliance and Institutional Requirements

As global regulatory scrutiny of stablecoins increases, compliance has become a key factor in stablecoin adoption. Blockchain ecosystems that support compliance requirements (such as Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations) may see higher adoption rates among institutional users and compliant stablecoin issuers.

In 2023, around 30% of stablecoin inflows on Ethereum were related to institutional transactions, primarily due to Ethereum's stablecoins (such as USDC) having regulatory compliance capabilities. In contrast, chains with a more lenient regulatory structure (such as Tron) mainly serve retail users and remittance-based use cases.

Algorand and Ethereum have positioned themselves as regulatory-friendly ecosystems. Algorand supports compliant stablecoins (like USDC) and has partnered with regulated financial institutions to ensure compliance. Ethereum, through Circle's USDC and MakerDAO's DAI, offers compliant options, making it a preferred stablecoin issuance platform with significant institutional interest.

As regulatory clarity around stablecoins continues to evolve, blockchain ecosystems that prioritize compliance may attract more institutional participation. For example, Avalanche's customizable subnets feature allows institutions to build regulated environments, which may appeal to stablecoin issuers that need to adhere to specific compliance standards.

5. Geographic and Regional Demand for Low-Cost Remittances

In regions with limited financial inclusion or high banking fees, stablecoins have provided a viable alternative for daily transactions and cross-border remittances. Ecosystems that can meet these market demands through low fees, high accessibility, and integration with payment providers are better positioned for stablecoin adoption.

According to the World Bank's 2023 report, global remittance flows have exceeded $700 billion, with stablecoins capturing an increasing share of cross-border transactions in countries with limited financial infrastructure. Blockchain environments that offer low transaction costs and fast processing have the potential to tap into this remittance market segment.

Tron is widely popular in regions such as Asia, Africa, and Latin America, where its low fees make it an ideal choice for cross-border remittances. Tron's network processes a significant volume of stablecoin transactions daily, especially USDT, which has been widely adopted in these regions as an overseas remittance tool that does not rely on traditional banking services. Tron's average transaction fee remains below $0.10, making it an ideal platform for remittance-based stablecoin usage.

The Binance Smart Chain (BSC), also known for its low fees and strong presence in Asia, is suitable for the remittance market. In these regions, Binance's exchange ecosystem has already established trust. Additionally, chains like Celo are targeting emerging markets through a focus on mobile financial services to promote the use of stablecoins among the unbanked or underbanked populations.

6. High Scalability

Layer 2 solutions have provided blockchain with an effective way to address high transaction costs while maintaining security and decentralization. Blockchains integrated with Layer 2 scaling solutions can support a larger volume of stablecoin transactions at a lower cost, attracting users who were previously excluded due to high Layer 1 network costs.

Ethereum-based Layer 2 protocols (such as Arbitrum and Optimism) have seen a total value locked (TVL) surpassing $5 billion by mid-2024. Stablecoins play a significant role in various DeFi applications and payments. Layer 2 solutions have reduced transaction costs by over 90%, making them highly attractive to stablecoin users.

Polygon is one of the leading Layer 2 scaling solutions, driving significant growth in stablecoins by providing Ethereum's security and lower fees. Platforms like Aave and Uniswap have deployed on Polygon to benefit from lower costs. Concurrently, the usage of USDC and DAI on Polygon has significantly increased. Similarly, the cost efficiency of Arbitrum and Optimism has attracted DeFi protocols dependent on stablecoins.

With more chains adopting Layer 2 scaling solutions, the adoption of stablecoins in these environments may increase, allowing users to access stablecoin functionality at a lower cost.

Potential Challengers

As global demand for stablecoins grows, emerging blockchain ecosystems such as TON (The Open Network) and Sui have shown immense potential for stablecoin adoption due to their unique infrastructure, target user base, and growth strategies. While mature blockchains like Ethereum, Tron, and BSC currently dominate stablecoin activity, TON and Sui are injecting significant differentiation and competitiveness into the stablecoin market through innovative approaches. We provide a detailed analysis of the potential of TON and Sui in driving stablecoin growth, compare them to current leaders, and examine the financial impact of stablecoin activity growth in these ecosystems.

TON: Driving Retail-Focused Stablecoin Adoption on the Telegram Network

TON was initially developed by Telegram and later handed over to the open-source community, evolving into a high-performance blockchain. TON currently has a market capitalization of around $5 billion, significantly smaller than Ethereum's $200 billion and BSC's $35 billion. Nevertheless, TON's potential lies in its unique integration with Telegram. With over 700 million monthly active users globally, Telegram's existing user base positions TON as a key contender for stablecoin adoption, especially in markets where Telegram is widely used for communication and peer-to-peer transactions.

Key Features Driving Stablecoin Adoption

1. Seamless Integration with Telegram:

TON's direct integration with Telegram enables stablecoins on its network to be highly accessible to Telegram users, facilitating seamless peer-to-peer transfers and payments. This setup is particularly advantageous in countries with limited banking infrastructure but widespread Telegram usage (e.g., Russia, Ukraine, Turkey, parts of the Middle East, and Southeast Asia).

Use Case: If stablecoins like USDT or USDC are widely adopted on TON, users could send stablecoins within the Telegram app with a single click. This integration could make stablecoins on TON as easy to use as Venmo or WeChat Pay, providing a low barrier to entry for users unfamiliar with blockchain.

2. Low Fees and High Scalability:

TON's sharding architecture supports low-cost processing of high transaction volumes, making it attractive for stablecoin transactions. The average transaction fee on TON is estimated to be less than $0.01, comparable to the cost efficiency of Tron and BSC. This cost-effectiveness could drive adoption for day-to-day transactions and micropayments, especially among fee-sensitive users.

TON's high scalability ensures that it can handle increased traffic without significant speed reductions or fee hikes, which is crucial for stablecoin usage in high-frequency transaction scenarios such as remittances and retail purchases.

3. Built-in Custody Options and User-Friendly Interface:

TON offers both custodial and non-custodial wallet options to cater to different types of users. The embedded custodial wallet in Telegram simplifies the user experience for the average user, while the non-custodial wallet serves security-conscious and asset-ownership-focused crypto-savvy users. This dual approach can increase adoption among different user groups, including retail users and more experienced crypto asset holders.

If TON successfully attracts stablecoins or launches its proprietary ecosystem stablecoin, it could capture a significant share of the retail and remittance markets. Given Telegram's widespread influence, TON has the potential to attract millions of new stablecoin users in Telegram's popular emerging markets.

If TON captures just 1-2% of the current global stablecoin market (valued at around $120 billion), it would bring about $12 billion to $24 billion in stablecoin market value growth within its ecosystem. This additional activity could elevate TON's market capitalization from $5 billion to $60-70 billion, positioning it as one of the top platforms for stablecoin transactions.

Building on top of Telegram's 700 million active users, even with just a 5% stablecoin adoption rate, TON could bring in 35 million users, a significant increase compared to the adoption rates of existing stablecoins on other blockchains. This user base will not only drive stablecoin transactions but also increase demand for other TON services, thereby fostering ecosystem growth.

TON's Value Proposition in Use Cases

TON's deep integration with Telegram has significantly boosted stablecoin activity. This vast existing user base gives TON an unparalleled audience reach that other blockchain ecosystems cannot match. By May 2024, the supply of Tether (USDT) on the TON blockchain has surged from $100 million to $1.2 billion, indicating continuous growth in user adoption within the Telegram ecosystem.

Telegram's penetration in regions with insufficient traditional banking infrastructure, such as Russia, Southeast Asia, and the Middle East, provides a practical alternative for TON-based stablecoins for peer-to-peer payments and remittances. If Telegram natively integrates stablecoins, users could seamlessly send funds, as easily as Venmo or WeChat Pay but with global coverage. This convenience could accelerate mainstream stablecoin adoption in underbanked regions.

TON's sharded architecture allows it to achieve high scalability while maintaining low transaction fees, with transaction costs typically below $0.01. This cost-effectiveness is crucial for small-value transactions and high-frequency retail use cases. For example, stablecoins on TON could be used for tipping, digital content payment, or small business transactions within the Telegram community. Furthermore, the low transaction costs on TON make it a strong contender in the global remittance market, especially in emerging economies. According to World Bank data, global remittance flows exceeded $700 billion in 2023, with stablecoins playing an increasingly important role in these cross-border payments. TON's integration with Telegram streamlines the remittance process, reducing costs to a fraction of traditional banking methods, making it an ideal alternative for millions of users worldwide.

Sui: A High-Performance Blockchain Focused on DeFi and Institutional Use Cases

Sui, developed by Mysten Labs, is a relatively new blockchain with a current market capitalization of around 8 billion USD. Despite being in its early stages, Sui has emerged as a strong contender for stablecoin adoption due to its high-performance capabilities and focus on DeFi. Compared to Ethereum and BSC, Sui has a relatively smaller market cap, but its specialized technology and appeal to institutions position it well for growth in the stablecoin and DeFi space.

Key Features Driving Stablecoin Adoption

1. Advanced Consensus Protocol supporting High Throughput and Low Latency

Sui utilizes the Narwhal and Tusk consensus protocols, supporting high transaction speeds and low latency. This design offers the ability for high transactions per second (TPS), making Sui an ideal platform for DeFi applications such as lending, borrowing, or complex trading scenarios that require high transaction speeds and reliability. The low latency also benefits stablecoin users needing instant settlement.

Use Case Example: High-frequency trading is a significant part of DeFi, with stablecoins playing a crucial role in quick collateral swaps and liquidity provision. Sui's high throughput may attract institution-grade DeFi protocols reliant on stablecoins, positioning it as a competitor to Ethereum in high-value DeFi transactions.

2. DeFi-Centric Ecosystem attracting Institutional Users

Sui is actively positioning itself as a blockchain focused on DeFi, with early applications in lending, decentralized exchanges (DEXs), and asset management. As stablecoins are essential to DeFi applications, Sui's emphasis on building a robust DeFi infrastructure may drive the demand for stablecoins used as collateral, liquidity pools, or exchange mediums.

Institutional Interest: Sui's programmable infrastructure allows for tailored compliance solutions, which could attract institutions seeking a secure, compliance-friendly environment for stablecoin transactions. This capability could facilitate partnerships with regulated stablecoin issuers, enhancing credibility and attracting institutional interest.

3. Security and Flexibility with Move Programming Language

Sui utilizes the Move programming language, designed for security and asset protection. Move's resource-oriented programming model minimizes error risks, ensuring a secure transaction environment that appeals to both retail and institutional users. Enhanced security could position Sui as a secure environment for high-value stablecoin transactions and complex DeFi protocols.

If Sui is able to capture 0.5-1% of the Ethereum stablecoin-driven DeFi market (estimated at around $400 billion), it would bring an additional $2 billion to $4 billion in stablecoin market cap value to the Sui ecosystem. Given Sui's current $8 billion market cap, this surge in activity could potentially boost its valuation to over $10 billion, achieving a doubling of market cap.

Meanwhile, Sui's architecture and compliance potential may attract institutional users who prioritize stability and security in the digital asset environment. If Sui becomes the preferred chain for institutional DeFi, significant capital inflows could be seen, thereby establishing its core position in the DeFi space alongside Ethereum and BSC.

Value Proposition of Sui in Use Cases

The use of the Move programming language has enhanced the Sui ecosystem, providing a secure environment for developers to build robust financial applications. Move's resource-oriented programming model reduces the risk of errors, ensuring the secure handling of digital assets within smart contracts. This makes Sui particularly attractive in institutional-grade stablecoin use cases focused on security and compliance. For example, programmable stablecoins deployed on Sui can support highly secure lending and borrowing protocols, enforcing collateral and repayment through algorithmic rules. This feature may attract large financial institutions looking to integrate stablecoins into their operations.

For instance, in November 2024, Sui entered into a strategic partnership with Franklin Templeton's digital asset arm, Franklin Templeton Digital Assets, a global investment firm. This collaboration aims to support developers within the Sui ecosystem and leverage Sui's blockchain protocol to deploy innovative technologies. Franklin Templeton's involvement highlights Sui's potential in driving institutional growth.

Sui's compliance-focused infrastructure makes it a viable platform for cross-border trade, where stablecoins can be used for real-time settlement of international transactions and trade terms can be enforced through smart contracts. This institutional appeal and flexibility enable Sui to compete with Ethereum in high-value stablecoin use cases.

Disclaimer: This article is for general information purposes only and does not constitute investment advice, recommendation, or an invitation to buy or sell any securities. The content of this article should not be relied upon as a basis for any investment decision and should not be used as a reference for accounting, legal, tax advice, or investment recommendations. It is recommended that you seek advice from your own advisors on any legal, business, tax, or other matters relating to investment decisions. Some information contained in this article may come from third parties, including companies invested in by funds managed by Aquarius. The views expressed in this article are solely the author's personal opinions and do not necessarily reflect the position of Aquarius or its affiliates. These views are subject to change at any time and are not guaranteed to be updated.

Reference:

https://www.coinbase.com/en-gb/institutional/research-insights/research/market-intelligence/stablecoins-new-payments-landscape

https://defillama.com/stablecoins

https://www.theblock.co/post/315362/ethereum-stablecoin-volume-hits-record-1-46-trillion-as-defi-demand-surges

https://remittanceprices.worldbank.org/sites/default/files/rpw_main_report_and_annex_q124_final.pdf

https://www.federalreserve.gov/econres/notes/feds-notes/primary-and-secondary-markets-for-stablecoins-20240223.html

https://www.chainalysis.com/blog/stablecoins-most-popular-asset/

This article is a contribution and does not represent the views of BlockBeats.

You may also like

The ten years of Cloud on the Air: From corner coffee to global financial infrastructure

From ByteDance to Financial Freedom: How did "Byte Brother" Leto develop his investment judgment skills to achieve a turnaround of 30 million?

OUSD False Cooperation Controversy? The Credit Game of Stablecoins and Endorsements by Giants

Trump, the best stock trader among U.S. presidents

Q-Day Countdown: Will Quantum Computing End Cryptocurrency?

Selling coins despite a loss of 55 million dollars, the faith in Strategy has reached the interest payment date

The cryptocurrency industry has become a traditional industry

Chip frenzy cooling down? Morgan Stanley's Wilson: Funds are shifting towards AI supercomputing giants like Microsoft and Amazon

$10,000 in TRUMP Token vs. $10,000 in Nasdaq: The "Trump Trade" That Actually Worked in 2026

Morning Report | Vitalik outlines Ethereum's long-term roadmap, Lean Ethereum will become the third major iteration; SK Hynix seeks to attract more AI investors by listing in the U.S

The impact of OUSD on Circle, Tether, and Paxos: not a single negative factor, but a more complex reshaping of competition

Li Feifei's latest long article: When video generation, robots, and NVIDIA all claim to be world models, we need a taxonomy

Blaming the desolation of the cryptocurrency world on the rise of AI is a form of intellectual laziness

Strategy Founder: The Next 10 Years of Bitcoin

Forbes Special Report: Stablecoin cross-border payments are faster now, but not cheaper yet

A valuation of 8 billion dollars, doubling in 8 months! What makes the crypto-friendly bank Erebor Bank stand out?

340 billion valuation: Li Yanhong's largest IPO, a seat in Kunlunxin's shares is hard to come by