Bitcoin Suisse 2025 Vision: Altcoin Total Market Cap to Grow Fivefold; Wealth Effect to Drive NFT Craze

Original Title: Bitcoin Suisse OUTLOOK 2025

Original Authors: Dominic Weibel, Denis Oevermann, Wolfgang Vitale, Matteo Sansonetti, Bitcoin Suisse

Original Translation: Wu Blockchain

Bitcoin Suisse, founded in 2013 and headquartered in Zug, Switzerland, is one of the earliest crypto financial service providers in Europe. The company offers a comprehensive range of services, including cryptocurrency trading, storage (such as providing secure wallet solutions), and custody services.

Foreword

1. The macroeconomic environment will fundamentally ease, supporting a soft landing.

2. Bitcoin (BTC) will become the strategic reserve asset of the United States, with other sovereign nations following suit.

3. The price of Bitcoin will surpass $180,000, nearing its all-time high.

4. Bitcoin's volatility will be lower than that of major tech stocks, indicating its gradual maturation into an institutional-grade asset.

5. Financial giants will launch institutional-grade Rollups on Ethereum.

6. An Ethereum staking ETF will cause post-market cap-adjusted fund flows to exceed Bitcoin's.

7. Bitcoin's dominance will peak by the end of the year.

8. Ethereum's monetary policy will become its anchor, accelerating its transition towards a "money" attribute.

9. The altcoin season will peak in the first half of 2025, with the market cap growing fivefold.

10. Solana will consolidate its position as a top-tier general-purpose smart contract platform.

11. The wealth effect will drive an NFT frenzy at the end of the cycle.

The U.S. election triggered what may be the largest paradigm shift in the history of digital assets. This marks a dramatic change in the regulatory environment, with the world's largest economy shifting from strict restrictive regulation to institutional embrace. It can be said that this is a major plot twist—from "Operation Chokepoint 2.0" suppressing banking services to exploring the establishment of a national strategic Bitcoin reserve, this process signals a fundamental shift in governmental stance on digital assets, far beyond the exploratory touches of a Bitcoin ETF or BlackRock's engagement with crypto assets.

The Cryptocurrency Political Action Committee (Crypto PACs) has deployed over $1.3 billion in expenditures in the election, securing a bipartisan victory and shaping the most cryptocurrency-friendly Congress in history. We believe the upcoming era will mirror the "late 90s Internet boom" in the cryptocurrency space. Back then, a relaxed regulatory environment and a friendly policy framework unleashed an innovation wave. However, as with all political promises, words are cheap, and we will closely monitor whether the new administration truly fulfills its commitments.

Against the backdrop of ETF records being broken and unprecedented institutional entry, traditional financial giants are not merely dipping their toes but diving headlong into the crypto space. However, the development landscape far surpasses traditional finance, with emerging areas such as DePIN, DeSci, and DeAI no longer just narratives but solutions to real challenges. Polymarket has bridged the gap, and the advancement of on-chain privacy tech as well as institutional-grade DeFi progress provides even more exciting reasons for the next wave of crypto adoption.

To translate the above content into a more actionable essence, the "2025 Outlook" pre-tests the coverage of the breadth of the crypto market, encompassing improved macroeconomic conditions and liquidity, crucial for sustaining the current crypto cycle, and Bitcoin's journey expected to reach a new all-time high. Further key themes include Bitcoin's rise as a strategic reserve asset, Ethereum's increased institutional adoption through staking, and the resurgence of altcoins and NFTs.

There are many topics worthy of in-depth exploration. Before delving into a detailed analysis, I would like to express my deepest gratitude to Denis Oevermann, Wolfgang Vitale, and Matteo Sansonetti; it is their outstanding research that made this report possible.

To our esteemed readers and friends: As we draw the curtains on another extraordinary year for the cryptocurrency space, thank you for your continued trust and attention to our research. While the holiday is a good time to rest, it is also advisable to keep an eye on market trends: all signs point to 2025 being even more exciting.

— — Dominic Weibel / Research Director

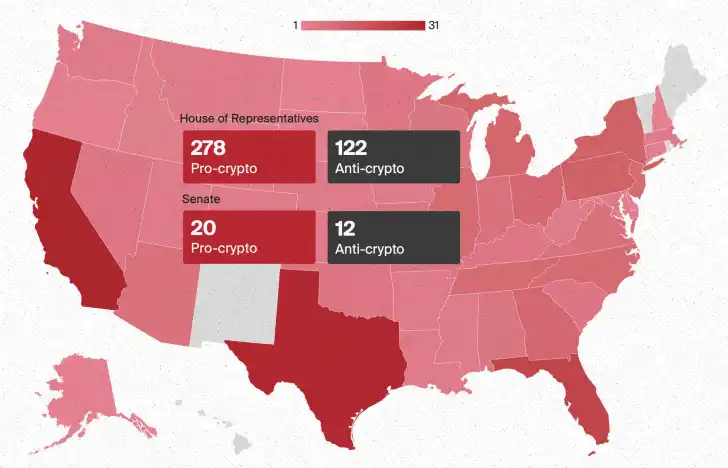

U.S. Elected Candidates Supporting Cryptocurrency

1. Fundamental Soft Landing Supported by Macro Conditions

The U.S. yield curve has been inverted for over 24 months, making it one of the longest periods on record. Although the 2-year and 10-year Treasury yield spread (2y10y) recently normalized, the 3-month and 10-year Treasury yield curve (3m10y) remains severely inverted, indicating ongoing market imbalances. Bitcoin (BTC) has shown significant sensitivity to these changes; for instance, in August 2024, when the 2y10y curve briefly normalized, Bitcoin intraday plummeted by $9,000 (-15%). As the short end of the yield curve gradually normalizes, continued volatility is expected, potentially creating short-term buying opportunities. However, the downside risk appears limited as market sentiment and economic conditions tend towards stability, provided major economic recession risks are avoided.

Based on historical patterns and the duration of the 2y10y inversion, the 3m10y curve may normalize by the end of the year, with the Fed's FOMC meeting on December 18 serving as a key catalyst. This normalization trend aligns with the improvement in financial conditions, such as the decline in the National Financial Conditions Index (NFCI), which has retreated from the 2023 tight state to a "normal" level. The reduced use of emergency liquidity tools (such as Bank Term Funding Programs BTFP) further indicates easing conditions. At the same time, global net liquidity shows signs of gradual improvement, which is a positive signal for market stability, although the current growth level remains significantly below the peak of 2021. Sustained liquidity growth is crucial to maintaining the upward momentum in the crypto market, especially as it unfolds in the latter stages of the bull market cycle.

So far, liquidity dynamics have been primarily driven by fiscal measures, with monetary liquidity lagging behind. However, there has been a policy shift post-election, transitioning from demand-side stimulus to a supply-side economic strategy. The new policy focuses on regulatory relaxation, targeted tax cuts, and lowering corporate funding costs to promote long-term productivity and employment growth. This strategic shift is expected to alleviate inflationary pressures while creating a more stable environment for economic growth. Additionally, increasing U.S. oil production to stabilize reserves and energy costs could strengthen deflationary trends and benefit energy-dependent industries, indirectly supporting broader markets. This will further drive monetary conditions and rate easing.

The evolving macroeconomic backdrop highlights a transition to a more sustainable growth model as supply-side measures replace the demand-driven strategies of recent years. This strategic shift, combined with liquidity improvement and stable financial conditions, places the crypto market in a favorable position for sustained growth. Bitcoin and other major crypto assets are poised to benefit from these favorable conditions, with the improving macro conditions likely driving stronger performance and unlocking significant growth opportunities within the current bull market cycle.

Global net liquidity is improving but still significantly below the peak of 2021.

Yield Spread and Yield Curve Normalization Impact

Global Net Liquidity vs. Global M2 Money

Global Net Liquidity: Refers to the sum of major central bank asset purchases and balance sheet expansions globally, hence being a key driver of financial market available liquidity. Contraction in global net liquidity often coincides with market weakness, while liquidity expansion drives overall economic growth and upward asset price trends.

2. Bitcoin Becomes the United States' Strategic Reserve Asset, with Other Sovereign Nations to Follow

Bitcoin is currently at a crucial stage in integrating into the global reserve strategy core. Against the backdrop of increasing fiscal uncertainty, geopolitical divisions, and a shift in the monetary order, we predict that Bitcoin will emerge as a key asset in national reserves. This trend will change the way nations hedge risks and exercise economic sovereignty, strengthening financial resilience through diversifying public fund allocation. Central banks' record gold purchases and sovereign nations' increasing experimental attempts with Bitcoin further indicate the growing importance of reserve asset diversification.

With the incoming Trump administration, we are observing a growing momentum in the United States adopting Bitcoin as a strategic reserve asset. The proposed "Bitcoin Bill" by Lummis suggests purchasing 1 million BTC, marking a significant milestone that could make the U.S. the largest Bitcoin holder nation, representing about 5% of the network's supply. This share, in dollar terms, is comparable to the U.S.'s share in global gold reserves. The U.S. government currently holds 200,000 Bitcoins through enforcement actions, which could serve as the starting point for a broad reserve strategy and provide precedent support for operations.

Not only is there federal-level drive, but state governments are also gradually following suit. For example, Florida and Pennsylvania are actively exploring direct Bitcoin purchases for their treasury departments, while Michigan and Wisconsin are opting for a more cautious approach through Bitcoin-related ETFs and trust funds. Additionally, as adoption indicators from the public and private sectors continue to rise, businesses are adding a significant amount of Bitcoin to their balance sheets, further highlighting Bitcoin's increasingly important role in financial management.

From a global perspective, Bitcoin's influence as a reserve asset is becoming more evident. Our assessment shows that Bitcoin has surpassed the pound to become the world's fifth-largest currency while ranking as the seventh-largest global asset. These milestones are significant. From a geopolitical standpoint, Bitcoin's neutral nature is increasingly favored, as seen with recent acknowledgments of Bitcoin as property by Russia and China.

As a hedge against potential USD instability and a force supporting the USD's dominant position, Bitcoin is seen as a remedy to address current financial challenges. Since 2000, the purchasing power of major fiat currencies has declined by over 70%, reinforcing the demand for a "hard monetary anchor." Furthermore, Bitcoin offers a crucial option to address the rising sovereign debt challenge. The U.S. federal debt has now reached a record $36 trillion, projected to increase to $153 trillion by 2054, and Bitcoin's compound annual growth rate (CAGR) may provide a potent tool for the government to offset the impact of debt growth.

The reserve asset status of Bitcoin has the potential to not only strengthen the financial resilience of the United States but also to counter hostile nations' de-dollarization efforts. Legislative and bipartisan interest, especially against the backdrop of evolving monetary conditions, foreshadows a future where Bitcoin may stand shoulder to shoulder with gold as a core pillar of strategic reserves.

The impact of Bitcoin achieving reserve asset status is difficult to quantify but could trigger a profound shift in the global monetary landscape. Similar to the price surge of gold in the following decade after Nixon abandoned the Bretton Woods system in 1971, Bitcoin may also undergo a similar currency repricing process as it transitions from a controversial fringe asset to a nationally adopted reserve asset. The reserve asset status may lead to a snowball effect, with sovereign nations racing to accumulate holdings, fundamentally altering Bitcoin's market dynamics and potentially disrupting the traditional four-year cycle pattern in the coming years. The key variables lie in timing and implementation strategy rather than the certainty of development direction.

Global Reserve Asset History

Bitcoin Supply Distribution

“Bitcoin can help consolidate the U.S. dollar's position as the global reserve currency while serving as a reserve asset to significantly reduce national debt.”

— — Senator Cynthia Lummis

3. Bitcoin Price to Break $180,000, Close to All-Time High

Entering 2025, we continue to observe the evolving dynamics of the Bitcoin market, in line with our peak cycle forecast first issued in November 2023. According to Bitcoin Suisse's Dynamic Cycle Risk and Dynamic On-Chain Cycle Risk models, along with comprehensive growth projections, Bitcoin is expected to reach a peak valuation of $180,000 to $200,000 in 2025, creating a new all-time high.

In early 2025, the Bitcoin price entered a stage of heightened risk accompanied by high dynamic cycle risk. However, from a cyclical perspective, the model did not indicate this as an ideal profit-taking opportunity. Since the beginning of the year, Bitcoin's price has ranged between highs of $50,000 and $60,000, followed by a sharp increase nearing $100,000. Concurrently, risk indicators suggest that the current price environment is more stable than at the beginning of the year.

Earlier this year, Bitcoin reached a nominal all-time high of around $73,000 (inflation-adjusted price still over 5% below the 2021 high of $67,000). While on-chain risk remains at a relatively high level, it has not yet reached a point where it would be advisable to take profits. It is worth noting that Long-Term Holders (LTHs) have shown some selling pressure, but this pressure has been offset by institutional investors, particularly the demand for Bitcoin ETFs. These ETFs have been absorbing several times the daily mining output since their launch.

Bitcoin currently represents only 0.2% of the global financial assets, significantly lower than traditional asset classes such as real estate, bonds, and gold. However, with increasing institutional adoption—especially significant actions that may be taken by countries like the United States—Bitcoin's trajectory could undergo a major shift, disrupting traditional markets and accelerating its exponential growth. With the current global asset total reaching $910 trillion, even if Bitcoin were to capture a 5% to 10% share of these assets, under unchanged conditions and ignoring the significant growth of global assets over time, the price of Bitcoin could increase by 25 to 50 times, reaching $2.5 million to $5 million per coin.

While this scenario is already quite significant, in the long-term outlook, this may just be a transitional phase. For instance, Michael Saylor predicts that by 2045, the price of Bitcoin will reach around $13 million per coin. In the short term, such adoption could trigger a "super cycle," driving Bitcoin's valuation to surpass $300,000 during this cycle, aligning with the upper limit predicted by current trend lines.

Bitcoin Suisse's Dynamic Cycle Risk Indicator and Dynamic On-Chain Cycle Risk Indicator

• Price Color Dot:

Plotted through Bitcoin Suisse's Bitcoin Dynamic Cycle Risk Indicator to assess the relative risk level of Bitcoin price levels.

• Bottom Oscillator:

Built based on Bitcoin's Dynamic On-Chain Cycle Risk Indicator to analyze the relative risk level of on-chain activity.

Bitcoin Dynamic Cycle Risk Indicator

The Bitcoin Dynamic Cycle Risk Indicator is a proprietary tool of Bitcoin Suisse used to evaluate the relative risk of Bitcoin price levels by analyzing key factors such as momentum, trend strength, and cryptocurrency inter-cycle dynamics. This indicator can be adjusted based on market conditions, maintaining a stable risk level during moderate price increases and reducing risk during sideways or downward price movements.

The Bitcoin Dynamic On-Chain Cycle Risk Indicator is a proprietary tool by Bitcoin Suisse used to evaluate the relative risk of Bitcoin on-chain activity by analyzing various individually optimized and adjusted on-chain risk indicators. Each indicator is specifically designed to reflect a dynamic cross-cycle, capable of independently identifying market tops and bottoms. This indicator dynamically adapts to market conditions, reducing risk during periods of subdued activity and increasing risk during periods of heightened on-chain activity.

Comparison of Bitcoin and Cryptocurrency to Global Financial Asset Market Cap

4. Bitcoin's Volatility Set to Fall Below Major Tech Stocks, Signaling Institutional-Grade Asset Maturity

Since its inception, a key characteristic of Bitcoin has been its significant volatility. However, this volatility has been steadily decreasing, and we believe new investment products may further narrow its price swings. The approval of the first Bitcoin spot ETF, along with regulatory clearance for related options listings, has attracted new capital into the Bitcoin ecosystem, improved infrastructure, and expanded the range of investment opportunities. Since late summer, Bitcoin ETFs have consistently represented around 5%-10% of the daily average Bitcoin spot trading volume.

The key drivers behind compressing Bitcoin volatility include: stable demand flows from institutional adoption, larger market cap leading to price inertia, systematic portfolio rebalancing flows from asset allocators, hedge funds' complex strategies dampening extreme swings, and the overall maturation of the asset class.

Additionally, the options market has played a crucial role in this trend. Historically, the options market has been shown to reduce the volatility of the underlying asset over the medium to long term through a combination of hedging activities and enhanced liquidity.

Professional investors may leverage the newly created market to amplify Bitcoin's inherent volatility. Through strategic trading techniques, they have the potential to exacerbate volatility in the short term.

We believe that ongoing regulatory developments surrounding Bitcoin will accelerate its position in the mature asset class. With continued compression of future volatility, we expect Bitcoin to further solidify its "digital gold" status and potentially reach volatility levels lower than high-tech stocks.

The decrease in Bitcoin volatility could enhance its risk-adjusted performance. Over the past year, Bitcoin's high returns have been accompanied by sharp swings, negatively impacting metrics like the Sharpe ratio. Since 2017, Bitcoin has seen an absolute return of about 7,000% with a Sharpe ratio of 1.108. In comparison, Tesla has had a return of around 2,000% with a Sharpe ratio of 1.101 during the same period, while NVIDIA has seen a return of 5,600% with a Sharpe ratio of 1.996.

The Decrease in Bitcoin Volatility and Its Double-Edged Sword Effect: As the asset matures, its stability metrics and institutional applicability are enhanced, while also weakening the historically asymmetric return potential of this asset class.

Bitcoin and Selected Stock Volatility Forecast

The chart displays the 30-day rolling volatility of four assets: BTC (Bitcoin), Meta, Tesla, and Nvidia. To reduce noise, Gaussian smoothing with a sigma value of 30 was applied. The shaded area represents the confidence interval of the average of Bitcoin and selected stocks. To ensure consistency, different assets used different percentiles: Bitcoin's confidence interval is based on the 80th percentile, while the traditional financial stock set uses the 95th percentile. The higher predictability of the traditional financial stock portfolio is attributed to diversification effects.

5. Financial Giants to Launch Institutional-Grade Rollups on Ethereum

Institutions are entering the crypto industry at an unprecedented pace. Stripe completed the largest acquisition in history by acquiring blockchain payments company Bridge; BlackRock quickly surpassed Grayscale to become the largest crypto fund by assets under management (AUM). Out of 22 major global financial institutions, 13 have begun researching the tokenization market, which is expected to reach $160 trillion by 2030. The adoption rate of Bitcoin ETFs is at a record pace, Swift has also initiated a pilot project for tokenized fund settlement, and countless other significant developments within the industry.

We believe that the conditions for institutional involvement are now ripe, and their next logical step is to deepen their integration with the Ethereum blockchain through a comprehensive Rollup implementation.

Ethereum provides undisputed high uptime, security, fairness, neutrality, and decentralization, making it the preferred platform for institutional on-chain use cases (such as stablecoins or tokenization). For example, BlackRock has launched its tokenized fund BUIDL, while Visa has announced its tokenized asset platform VTAP and plans to launch a pilot project in 2025.

From a technical standpoint, the implementation of EIP4844 has been widely successful, reducing Rollup transaction costs to less than 1 cent, with daily Rollup transaction volume reaching 30 million. Base, Arbitrum, and Optimism are the most funded Rollups in the industry since the beginning of the year, with TVL (total value locked) growing by over 60%. Additionally, significant cross-chain interoperability improvements are forthcoming, allowing these institutions to seamlessly access Ethereum, the most capital-dense smart contract ecosystem.

In addition to market expansion, efficiency gains, and overall first-mover advantage, institutions can also tap into a whole new revenue stream through Sequencing (including MEV and transaction fees). Based on existing Rollup benchmarks, a Sequencer's annual income can reach as high as $80 million.

Proprietary Rollups can also offer institutions full control over latency, consensus rules, token standards, and execution environments, while supporting built-in compliance features such as mandatory KYC or AML checks, blacklisting capabilities, and protocol-level automated regulatory reporting.

Furthermore, the tokenization of ETFs and payment-related opportunities can further complement the Sequencer's revenue streams. Cross-border payments, cost savings, short settlement windows, built-in forex functionality through DeFi integration, B2B payments, programmable payment schedules, and real-time treasury operations all provide robust support for Rollups. The packaging of equities and ETFs can also help institutions access emerging markets, as 90% of the global population is currently underserved by brokerage services. Recent institutional funds entering DeFi, such as the BUIDL fund via Elixir's deUSD protocol, indicate a clear trend in this direction.

Lastly, history has shown that attempts at private blockchains have failed to materialize successfully, while Rollups on Ethereum present a natural evolutionary path. This model creates a vertically integrated stack where institutions can control both the infrastructure layer and the financial product layer running on top of it. The advantages are self-evident: 2025 will be the institutional Rollup's prime year.

Tokenization of Real-World Assets (excluding stablecoins) across Industries

Revenue and On-chain Profit of Top-tier Rollups (In the Past Year)

On-chain profit measures a Rollup's profitability by comparing gas fee revenue to the data and proof submission costs on Ethereum. Profitability gains come from high block space demand (supporting premium pricing) or operators increasing the base fee multiplier.

Institutional Adoption of Cryptocurrency

The current conditions are highly favorable for institutional participants to take the next step by fully deploying Rollup on Ethereum, further deepening their blockchain integration.

6. ETH Staking ETF to Drive Market Cap-Weighted Inflows Beyond BTC

Despite Bitcoin ETF witnessing $32 billion in net inflows and IBIT nearing $50 billion AUM in just 225 trading days setting a record, we anticipate a structural shift in fund flows toward ETH ETF post-election. Despite underwhelming performance since ETF launch, fundamentals indicate ETH is displaying increasingly attractive risk-return characteristics amidst surging institutional participation. November marked a turning point for ETH ETF capital inflows, achieving net inflows for the first time since July launch, with single-day inflows reaching as high as $3.329 billion, surpassing Bitcoin's $3.2 billion. Furthermore, recent inflows have caught up with Bitcoin on a market cap-weighted basis.

We believe that ETH's relatively poor performance post-ETF approval mainly reflects institutional prefence for Bitcoin's mature narrative and higher awareness, while also being impacted by regulatory hurdles surrounding ETH ETF staking rewards. Regulatory uncertainty and the opportunity cost of not receiving staking rewards have significantly limited institutional inflows. However, this gap sets the stage for a strong rebound once the bottleneck is cleared. We anticipate rapid approval of ETH Staking ETF under the new Trump administration, unlocking a 3%-4% yield. This feature caters to institutional allocators' needs and is particularly appealing in a declining interest rate environment. We predict staking rewards will significantly benefit Ethereum and become a key catalyst driving ongoing fund flows into the ETH ETF. Furthermore, strategic acquisitions by staking service providers (such as Bitwise) further indicate these participants are actively preparing for this outcome.

In addition to the ETH Staking ETF, we expect more cryptocurrency ETF approvals by 2025, including SOL and XRP, sparking a broader discussion on the classification of L1 as commodities. However, Ethereum's unique position — as a regulated, yield-generating asset with a validated institutional adoption rate — may still remain unchallenged. Compared to Bitcoin, Ethereum is currently in the early stages of institutional adoption lifecycle. With institutional funds rotating only between the two major crypto assets, Ethereum's supply dynamics strongly hint at its potential future value appreciation. Over the past 12 months, over 70% of the ETH supply has remained dormant, while staking participation rates hit an all-time high.

In summary, we predict that the post-election wave of institutional crypto allocation will be primarily driven by returns, leading to a reversal in fund flows. The favorable intersection of regulatory tailwinds, yield potential, and supply dynamics will allow the ETH ETF to surpass BTC in market cap-weighted inflows by 2025.

Performance Since ETH ETF Launch

ETH ETF Cumulative Inflows and Daily Fund Flow

ETH and BTC ETF Market-Cap-Adjusted Fund Flows

7. Bitcoin Dominance to Peak by Year-End

Bitcoin's market dominance is expected to reach its peak for the current cycle at the inflection point in 2025, signaling a significant shift in the crypto market structure. While Bitcoin's absolute value will continue to rise, its dominance is projected to decline in the late stage of the bull market as capital rotates towards investing in other crypto assets (i.e., Altcoins). This pattern aligns with the market cycle being driven by Bitcoin halving events: Bitcoin's dominance typically surges in the early stages but as the bull market progresses to its final phase, Altcoins start taking the lead, causing the Bitcoin dominance to decrease.

Ethereum (ETH) and Solana (SOL) are key assets expected to outperform Bitcoin against the BTC trading pair during this phase. Unlike many Altcoins where the USD valuation tends to remain relatively stable, their BTC ratio tends to approach zero over time. In contrast, the performance of ETH and SOL acts like an oscillator, maintaining resilience in their relative strength against Bitcoin. This resilience reflects their increasing importance in the broader crypto ecosystem, providing investors with a more diversified growth trajectory compared to Bitcoin.

The anticipated decline in BTC dominance aligns with historical trends and broader macroeconomic dynamics, including liquidity cycles, the halving process, and the characteristic slowdown in market sentiment post-halving and post-elections. With improved liquidity, the attractiveness of high-risk assets as investments increases, amplifying the trend of capital flowing towards Altcoins and enhancing their outperformance. This structural shift highlights the role of Altcoins in the late stage of the cycle, with their relative returns expected to surpass Bitcoin.

While Bitcoin is expected to maintain strong returns, the major gains in the late bull market phase are projected to come from Altcoins. This scenario reflects a maturing market structure where capital is more inclined towards high-risk opportunities during bullish sentiment. As Bitcoin dominance decreases, Altcoins will capture a larger market share, prompting investors to reassess portfolio strategies in the final stages of the bull market. Following the conclusion of this stage, Bitcoin's dominance is expected to resurge, laying the foundation for the next market cycle.

Bitcoin Dominance Trend

Ethereum (ETH) and Solana (SOL) Compared to Bitcoin (BTC) in Terms of Cyclical Volatility

8. ETH's Monetary Policy Anchor, Accelerating Its Monetization Process

Despite strong voices supporting a modification of ETH's monetary policy, the issuance rate of Ethereum staking rewards will not change in 2025, nor will there be consensus to incorporate a modification into the expected 2026 hard fork. During 2024, several Ethereum researchers have questioned the sustainability of the staking economy and proposed adopting a new issuance curve, setting a cap on the staking ratio, or introducing mechanisms to stabilize it near the target value. These proposals aim to address the risks posed by an excessively high staking ratio, including unnecessary inflation and pressure on the network. In extreme cases, ETH could be replaced by a single-dominant liquidity staking token (LST), leading to an unacceptable impact on Ethereum.

We believe that it is crucial for ETH to maintain its role as a globally trusted neutral currency settlement, thus expressing concerns about an excessively high staking ratio. Nevertheless, in pursuit of the monetization goal, there are also opposing voices that argue any issuance adjustment may weaken its perception as a "sound money" (especially when compared to Bitcoin's fixed monetary policy).

Although ETH's issuance policy has changed several times, most notably with the introduction of staking, the rise of competitors like Celestia and Solana in 2024 has made preserving ETH's monetary attributes even more critical. While competitors can swiftly optimize in specific areas, the process of their new currencies being accepted as money is much more challenging.

Due to the importance of this decision and the disagreement on how to achieve monetization, it is expected that the Ethereum community will have difficulty reaching a consensus on changing the issuance policy by the end of 2025. Furthermore, even if an ETH staking ETF is approved, we do not expect the staking ratio to reach the levels demonstrated by most PoS chains. We anticipate the staking ratio to increase at a growth rate similar to last year's (+18%), reaching approximately 33% in 2025. The relatively lower staking ratio and the integration of validators post EIP-7251 will further reduce the urgency for policy changes.

We believe that the consolidation of ETH's 2025 monetary policy will have a positive impact on its valuation and help differentiate it from other platforms. However, we do not rule out potential adjustments in the future after reaching a broader social consensus, thus defining the "final form" of the staking economy.

Example: Proposed Changes to Issuance Curve and Issuance Yield

The issuance yield is lower than the staking yield as it does not include transaction fees and MEV

ETH Total Supply and Staking Ratio Changes

Comparison of staking ratios across major PoS networks

9. Altcoin Season to Peak in First Half of 2025 with Total Market Cap Expected to Grow 5x

As the crypto market enters a critical phase in 2025, the Altcoin season is approaching. Historically, this transition usually occurs in the later stages of a Bitcoin-dominated bear market, where Altcoins continue to underperform (shown in the dark gray area in the chart). However, the upcoming market rotation will drive capital (mainly from Bitcoin) towards Altcoins, marking the beginning of a decisive and significant Altcoin season.

The most explosive Altcoin seasons typically coincide with the final push of a Bitcoin bull market, usually occurring as Bitcoin reaches its cycle peak. This cycle seems to be no exception. Bitcoin is expected to approach a market cap of 4 trillion USD, with its dominance waning, creating ideal conditions for Altcoins to outperform. Current trends indicate that the first half of 2025 will see the strongest and most significant Altcoin season of this cycle, driven by capital rotation and high-risk appetite, particularly evident as Bitcoin consolidates near its peak.

By using Bitcoin and Ethereum's market cap targets as benchmarks, the potential scale of Altcoin's performance can be clearly seen. Assuming the total crypto market cap for this cycle reaches around 15 trillion USD, with Bitcoin expected at 4 trillion USD and Ethereum at 1 to 1.5 trillion USD, this would leave around 10 trillion USD of allocation space for Altcoins. Currently, TOTAL3 (i.e., Altcoin total market cap excluding Bitcoin and Ethereum) is only 1 trillion USD, indicating that as the cycle matures, the Altcoin market as a whole could have as much as a tenfold growth potential.

The peak of Bitcoin's market cap, Ethereum's scalability, and the anticipated capital flow into Altcoins collectively form the basis for a profound Altcoin season in the first half of 2025. This period will offer significant opportunities for outsized returns, with some assets poised for exponential growth. As market dominance shifts, actively positioning and diversifying into Altcoins will be key to capturing the full potential of this high-growth phase.

Altcoin Season Index: Pointing to a Recent Significant Increase in Altcoin Returns

Altcoin Season Index: Measures whether the top 50 cryptocurrencies (excluding stablecoins) have outperformed Bitcoin over a certain period of time. When the index value is above 75, it indicates the onset of an Altcoin season; when it is below 25, it reflects Bitcoin dominance.

TOTAL3: The total cryptocurrency market capitalization excluding Bitcoin and Ethereum, essentially representing the market cap of all Altcoins.

Market Cap Forecast for Bitcoin, Ethereum, and Altcoins: Pointing to Future Multi-Fold Growth

10. Solana Solidifies Its Position as a Top-tier General-Purpose Smart Contract Platform

By 2024, Solana will emerge as a strong competitor to Ethereum in terms of real economic value (REV: transaction fees + MEV tips) and recognition from founders, investors, and users. We anticipate that with continued infrastructure improvements, Solana will maintain its advantage in the fiercely competitive environment in 2025.

With a fast iteration cycle, a strong core development team, and consistency in its value proposition and optimization strategy, Solana is currently well-positioned to enhance its network effects. However, next year it will face intense competition from Ethereum and other existing platforms (such as Aptos, Sui) as well as emerging platforms (such as Monad, MegaETH). High throughput and low fees may no longer be significant differentiators, so while 'increasing bandwidth and reducing latency,' critical improvements must be made at the foundational level.

The most anticipated upgrade in 2025 is the maturity of Firedancer, which will make Solana a more robust multi-client network. The Firedancer codebase will be separate from Agave, significantly reducing the risk of chain client failures, allowing validators to easily switch clients without waiting for issues to be resolved. Firedancer has been running on the mainnet in non-voting mode, enabling the team to collect data and test new features and optimizations.

Other infrastructure improvements will focus on several key areas:

• Mitigation of state growth: Addressing state growth by applying state compression technologies.

• Handling State Contention: Improving state contention issues globally by adopting a central transaction scheduler.

• Development of zk-rollups: With the recent introduction of dedicated system calls, more zk-rollups are expected to emerge.

• Improvement of Tokenomics: By reallocating priority fees to stakers (SIMD-0123) and continuing discussions on reducing the issuance rate.

• Scalability Enhancement: Enhancing scalability through asynchronous execution techniques and advancements in hardware capabilities.

• Strengthening Anti-censorship Capability: Enhancing anti-censorship capability through the implementation of a multi-leader mechanism.

• Lightweight Full Node Client Development: Continuing to advance the Mithril project to reduce hardware requirements.

While we do not expect to achieve all of these improvements by 2025, the shift from "rapid iteration, break things to make them better" towards a more strategic focus on foundational improvements by independent teams gives us confidence in Solana's sustainable success as a top-tier general-purpose smart contract platform. This success will be reflected in Solana's continued position as the preferred platform for DeFi and DePIN founders and will be more attractive to institutional-grade token issuers, which is crucial for realizing the potential of a global, permissionless, and efficient state machine.

Solana and Ethereum's Monthly Realized Economic Value

11. The Wealth Effect Will Drive NFT Momentum at the End of This Cycle

In recent years, the NFT market has experienced a significant retracement, where market expectations diverged from reality. We expect this trend to reverse in the later stages of this cycle, primarily driven by industry-wide wealth effects and capital rotation. While the performance of most NFT collectibles may still remain subdued, we believe that top-tier collectibles (such as CryptoPunks or Fidenzas) will rightfully establish themselves as social identifiers in the crypto space and high-end digital art, especially generative art. Underpinned by blockchain, generative art has found an ideal platform for expression, demonstrating the value of durable, irreplaceable, and ownable digital content through verifiable scarcity and on-chain provenance.

Projects like Pudgy Penguins have recently garnered more attention, being the second-largest NFT project by market cap, bolstered by the upcoming launch of its PENGU ecosystem token. In the current cryptocurrency culture trend that leans notably towards MemeCoins, the memetic nature of PENGU may surprise the market. Additionally, as the most successful consumer brand in the crypto space, the launch of the parent company's Abstract Chain may further accelerate its momentum.

The increase in trading volume in November and the recent performance of collectibles seem to indicate early signs of this trend. Magic Eden has become the first major NFT platform to complete a valuation event, and OpenSea may also be brewing a similar event. These events could enhance the stickiness and liquidity of the NFT market. Driven by these catalysts, we expect a significant appreciation in the value of related NFT collectibles. Similar to the previous cycle, we observe that NFTs tend to lag in performance before the market frenzy peaks, so the late-stage wealth effect may once again trigger a new wave of demand for highly scarce collectibles.

We predict that early Art Blocks collectibles will naturally benefit from this momentum. These collectibles combine historically significant on-chain generative art, recognition from renowned artists, validated collector demand, and true scarcity. Furthermore, these collectibles have maintained a relatively high price floor in bear markets and are expected to benefit in the next stage of market maturation, especially those that represent key moments in digital art history.

With the rise of a younger generation more familiar with digital technology, this trend may be further enhanced in future cycles.

Historical Performance of CryptoPunks (Priced in ETH and USD)

Historical Performance of Fidenzas (Priced in ETH and USD)

You may also like

Morning Report | OpenAI has submitted an S-1 registration statement draft to the U.S. SEC; Morpho completes $175 million financing

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

Morning Report | OpenAI has submitted an S-1 registration statement draft to the U.S. SEC; Morpho completes $175 million financing

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.